Geopolitical tensions have become an increasingly persistent feature of the global news cycle. Wars, sanctions, elections, trade disputes, and countless other escalations can make it feel as though markets are standing on unstable ground.

While this does not diminish the human impact of such events, stepping back from the immediacy and examining the historical record through an investment lens often reveals a more balanced picture than headlines suggest.

Over modern financial history, markets have navigated world wars, oil shocks, terrorist acts, financial crises, political upheavals, and shifting global power structures. While geopolitical events often create short-term volatility, the long-term behaviour of diversified equity markets has been remarkably resilient.

Recognising the distinction between short-term reaction and long-term outcome is therefore central to navigating periods of heightened geopolitical tension.

Immediate shock versus longer-term outcomes

History shows that major geopolitical events typically trigger an initial market reaction.

Equity markets often fall in the days or weeks following a significant escalation. Risk assets decline, volatility rises, and investors seek perceived safety in more traditionally defensive assets such as gold.

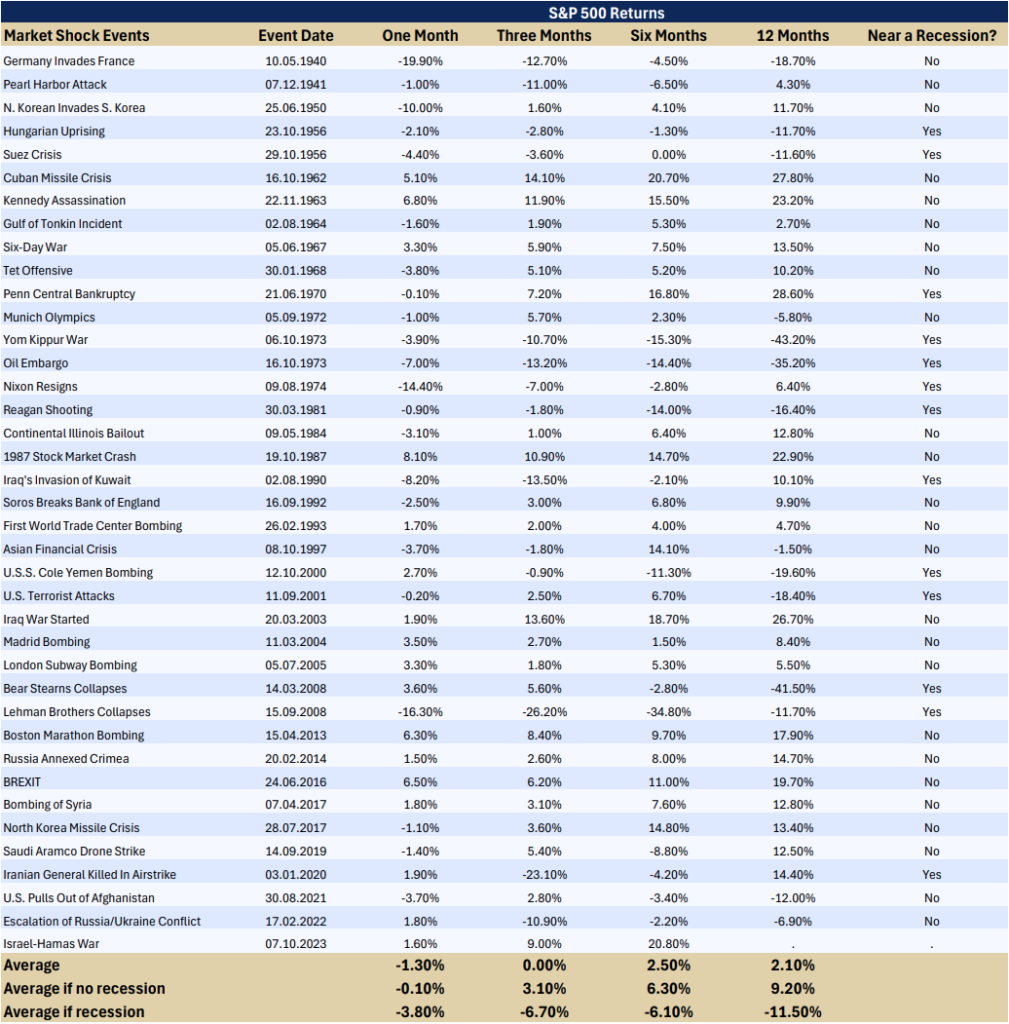

However, analysis of multiple historical episodes since the mid-twentieth century shows that the average short-term downturn following a geopolitical shock has been limited in its magnitude.

Markets frequently reached their low within weeks rather than months, with losses often recovered within a comparatively short period.

Importantly, when equity returns were assessed 6 to 12 months after major geopolitical events, broad, large-capitalisation markets often largely stabilised and resumed their prevailing trend.

Read to the end of this article to view the data behind these figures.

This does not mean that geopolitical events are irrelevant to markets or their broader implications. Rather, it reflects the market’s tendency to reprice risk rapidly, absorb new information, and then refocus on earnings, interest rates, and underlying economic fundamentals.

From a long-term investor’s perspective, the initial shock has historically been more visible than lasting.

Geopolitics is not without risk

As with most historical market patterns, exceptions inevitably arise.

The oil embargo of the 1970s is one such example. Energy shortages were prolonged, inflation accelerated, productivity declined, and the global economy entered a period of stagflation. Equity markets faced sustained pressure not solely because of the geopolitical event, but because it fundamentally altered the macroeconomic environment in the years following.

By contrast, more recent energy shocks have tended to be far shorter lived. Global production dynamics, alternative supply sources, and more flexible energy markets have limited the duration of disruption.

The distinction lies not in the geopolitical trigger itself, but in the economy’s ability to adapt. Where disruption is severe and sustained, permanently constraining productive capacity, the impact can be prolonged. Where supply chains, technology and capital flows are able to adjust, the shock is more likely to be absorbed over time.

Global markets versus local markets

Global equity markets, by their nature, are diversified across regions, sectors and currencies. Exposure is not concentrated in any single economy or political system, which can in turn lessen the impact of country-specific disruptions.

Local markets, however, tell a different story.

Where geopolitical events directly affect trade routes, energy access, supply chains, or regulatory frameworks, regional asset prices may respond more drastically.

Such pressures can emerge through several channels:

- Operational disruption, including higher costs, supply chain dislocation, and security concerns for locally exposed businesses.

- Earnings concentration risk, where companies reliant on domestic revenues experience greater volatility than globally diversified peers.

- Currency weakness, as capital reallocates internationally, increasing funding costs and financial pressure.

In these situations, while global markets may experience spill over effects through trade, supply chains, or investor sentiment, the most acute pressure is typically concentrated locally.

The impact of regional disruption reinforces the role global diversification has historically played in absorbing localised shocks and improving portfolio resilience.

What this means for you

Periods of geopolitical tension are inherently unsettling. Human consequences are often grave, and market reactions can heighten uncertainty, particularly while events are still unfolding.

However, history suggests several consistent patterns:

- Broad, diversified equity markets have generally absorbed geopolitical shocks without permanent damage.

- Local markets and concentrated exposures can experience prolonged effects.

- Volatility tends to spike in the short-term but has historically normalised over time.

While this does not eliminate investment risk, it reinforces the importance of maintaining a disciplined approach.

Portfolios that are globally diversified and aligned with long-term objectives have historically proven more resilient than concentrated exposures, as markets over decades have demonstrated an ability to adjust, adapt, and continue functioning through periods of significant geopolitical change.

Do you need a helping hand?

Whether you are reviewing your exposure to global markets, reassessing your capacity for risk, or considering how geopolitical uncertainty may affect your portfolio,

get in touch with us today and book your initial, no-cost and no-obligation meeting.

Send us an e-mail to contactus@pattersonmills.com or call us direct at +44 (0) 1908 503 741 and we shall be pleased to assist you.

To see the raw data mentioned in this article, we provide the table below.